Published March 3, 2026

The VA Loan Benefit You Earned and How to Use It

The VA Loan is one of the most powerful home financing tools available today, yet it is also one of the most misunderstood.

The VA Loan is a mortgage program backed by the U.S. Department of Veterans Affairs. The VA does not actually lend the money. Instead, it guarantees a portion of the loan, which reduces risk for lenders. Because of that guarantee, qualified veterans and service members are able to access some very strong advantages.

One of the most well known benefits is that most eligible buyers can purchase a home with no down payment. For many families, that alone removes the largest barrier to homeownership. In addition, VA Loans do not require private mortgage insurance. That can mean significant monthly savings compared to other loan types. Interest rates are often competitive, and the program is designed to offer flexible guidelines to support those who have served.

There are still many myths surrounding VA Loans. Some believe they take too long to close. In reality, the timeline depends on the lender and the preparedness of the transaction. With the right team in place, a VA Loan can move just as efficiently as any other loan. Others believe sellers will not accept VA offers. In truth, strong terms, proper presentation, and experienced representation matter far more than the loan type itself.

Another common misconception is that the VA Loan can only be used once. In many cases, entitlement can be restored and reused, allowing veterans to use this benefit again in the future.

It is also important to understand how VA entitlement works. Entitlement is the amount the VA guarantees on your behalf. Many veterans have full entitlement, which means there is no official loan limit and no required down payment as long as you qualify with your lender. If you currently have a VA Loan and have not restored your full entitlement, you may still be able to have more than one VA Loan at the same time. The key requirement is that each property financed with a VA Loan must be used as a primary residence when purchased.

When entitlement is partially used, there is a remaining entitlement amount available. The VA typically guarantees up to twenty five percent of the loan amount. If you choose to purchase above the amount your remaining entitlement supports, you can still do so, but you may be required to bring additional funds to closing to cover the difference. This is where having a knowledgeable lender and agent matters, because the math and structure need to be correct from the start.

Let’s say a veteran previously used part of their entitlement to purchase a home and still has a remaining entitlement amount available. The VA generally guarantees twenty five percent of the loan amount. If the county loan limit in the area is five hundred thousand dollars, the full guaranty at that level would be one hundred twenty five thousand dollars.

If the veteran has only seventy five thousand dollars of entitlement remaining and wants to purchase a home for four hundred thousand dollars, the lender will calculate how much additional coverage is needed to meet that twenty five percent guaranty. If the remaining entitlement does not fully cover that threshold, the buyer may need to bring a down payment to closing to make up the difference.

On the other hand, if the veteran has full entitlement restored, there is no official loan limit cap for zero down financing. That means they can purchase above traditional county limits without a required down payment, provided they qualify based on income, credit, and lender guidelines.

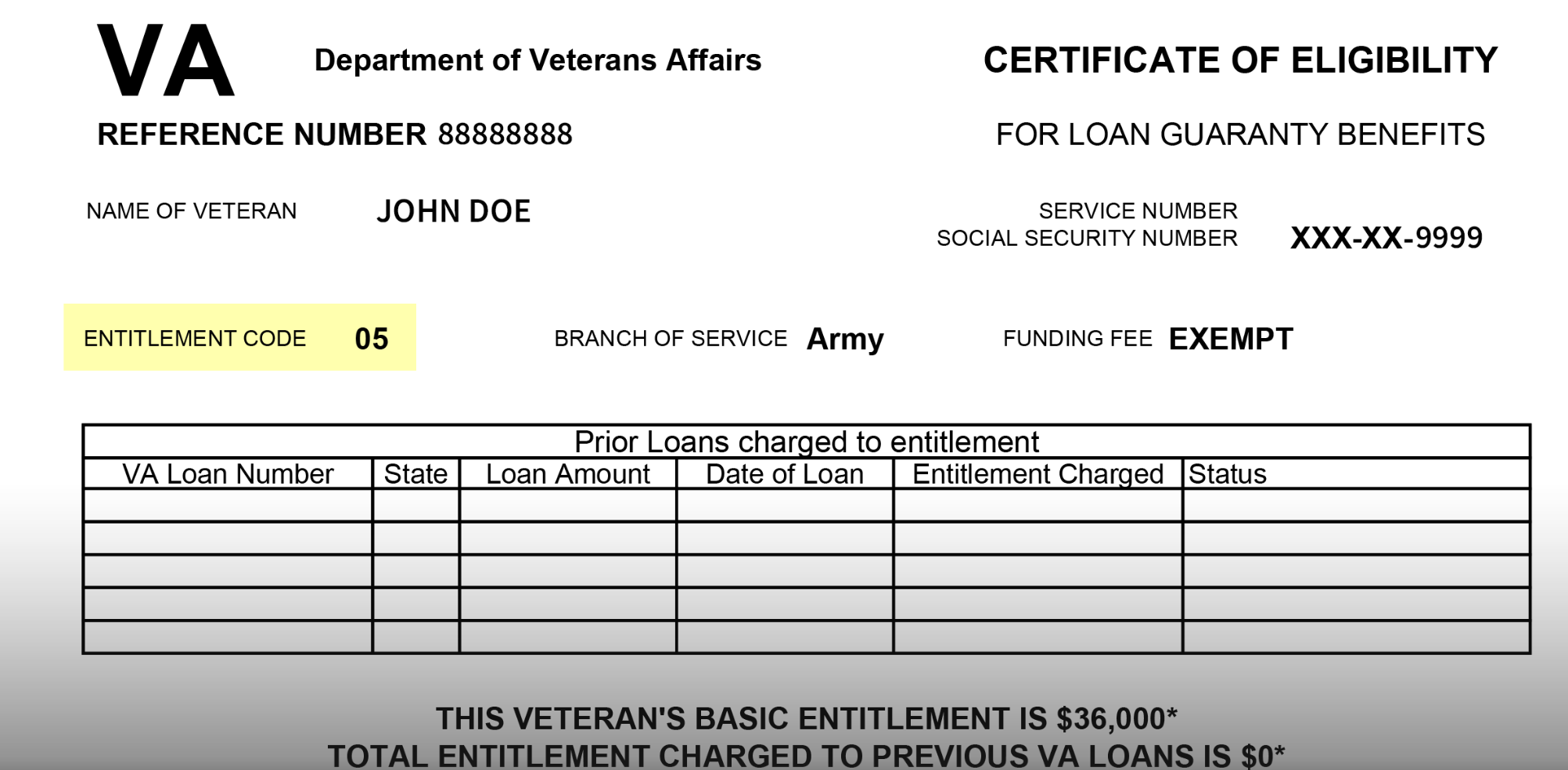

This is why reviewing your Certificate of Eligibility and understanding your current entitlement status is so important. Two veterans with different entitlement situations can have very different purchasing power, even if their income and credit look similar.

Eligibility is based on length and type of service. Veterans, active duty service members, certain National Guard and Reserve members, and some surviving spouses may qualify. The first step is obtaining a Certificate of Eligibility, which confirms access to the benefit.

For me, this is not just a financing option. It is personal. I was raised by a stong man who served in the Army, and I understand that this benefit was earned through sacrifice. Helping veterans and military families use their VA Loan wisely is a responsibility I take seriously. It is also one of the reasons I am affiliated with Homes for Heroes, a program that provides additional savings to those who serve.

If you are a veteran or active duty service member and have questions about how your VA Loan works, I would be honored to walk through it with you. Whether you are buying your first home, moving up, downsizing, or exploring your options, understanding your benefits is the first step toward making a confident decision.

You served our country. This benefit was earned. Let’s make sure you use it well.